Not included in these calculations, but also important to note, is that data centers have a refresh cycle where servers and hardware generally must be replaced every 2-5 years. For states heavily dependent on sales and use tax, those replacements trigger a repeated round of revenue.6

Direct Impacts

To produce the direct effects by industry type, the team gathered employment data for each development to serve as the primary input.7 Once appropriately scaled, each employment estimate was run through the Bureau of Economic Analysis (BEA) RIMS II EIA model to produce annual economic impacts.

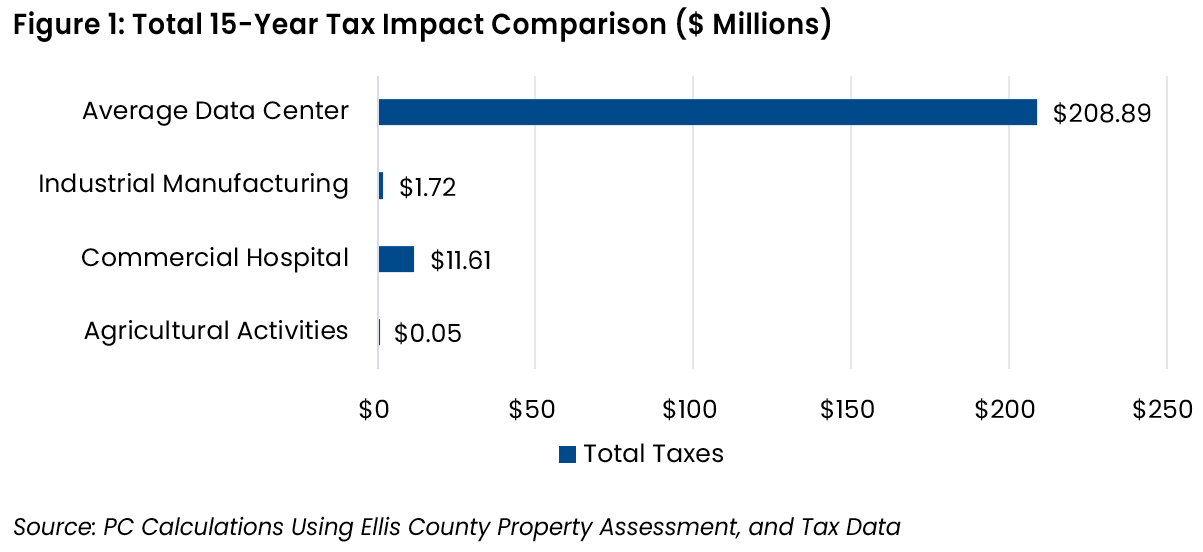

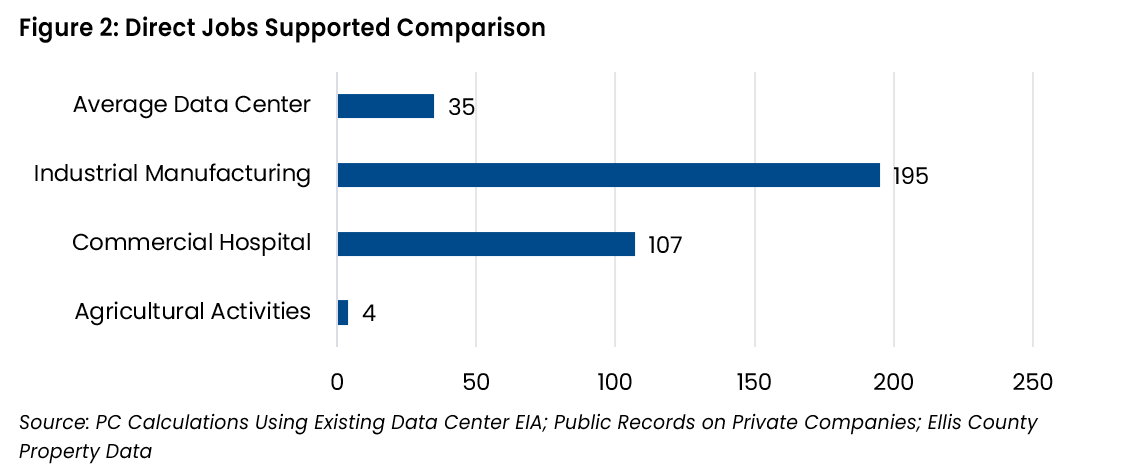

Figure 2 illustrates the differences in direct employment levels across each type of development. These findings represent the first metric that many community members and economic development professionals consider when assessing the full economic impact of a project in their region.

An Average Data Center is expected to support around 35 direct jobs. However, due to differences in labor intensity by industry, a manufacturing facility of comparable size is estimated to support 195 direct jobs. This is nearly six times the number of direct jobs supported by an Average Data Center (even accounting for the scale difference). We also expect a hospital to support roughly three times as many jobs as an Average Data Center.

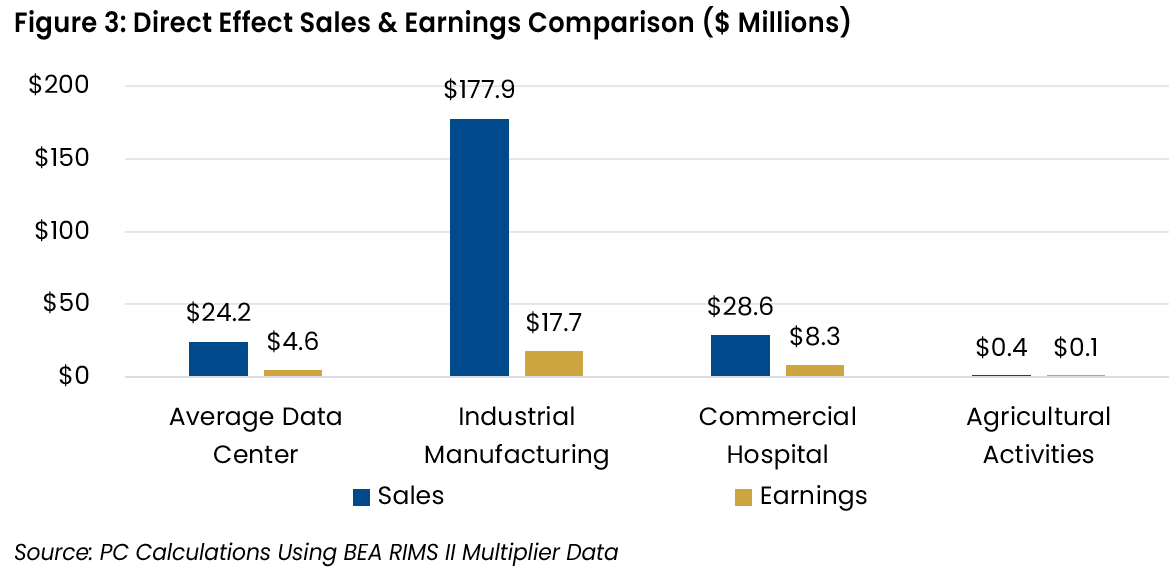

Using the BEA’s EIA model, PC estimated the direct economic output (sales) and earnings for each development type. An Average Data Center is expected to produce $24 million annually in sales (Figure 3). In contrast, we estimate a manufacturing facility to generate $178 million. This is seven times the output of the Data Center. Similarly, we project a typical hospital to outproduce an Average Data Center, generating $29 million in output.

The results for earnings are similar. A manufacturing facility is expected to outproduce the Data Center in economic output and earnings, though the gap for earnings is smaller.

Total Impacts

At the total impact level, additional multiplier effects are taken into account. Specifically, these include the additional economic impacts generated for other businesses in the region by an Average Data Center, manufacturing facility, or hospital.

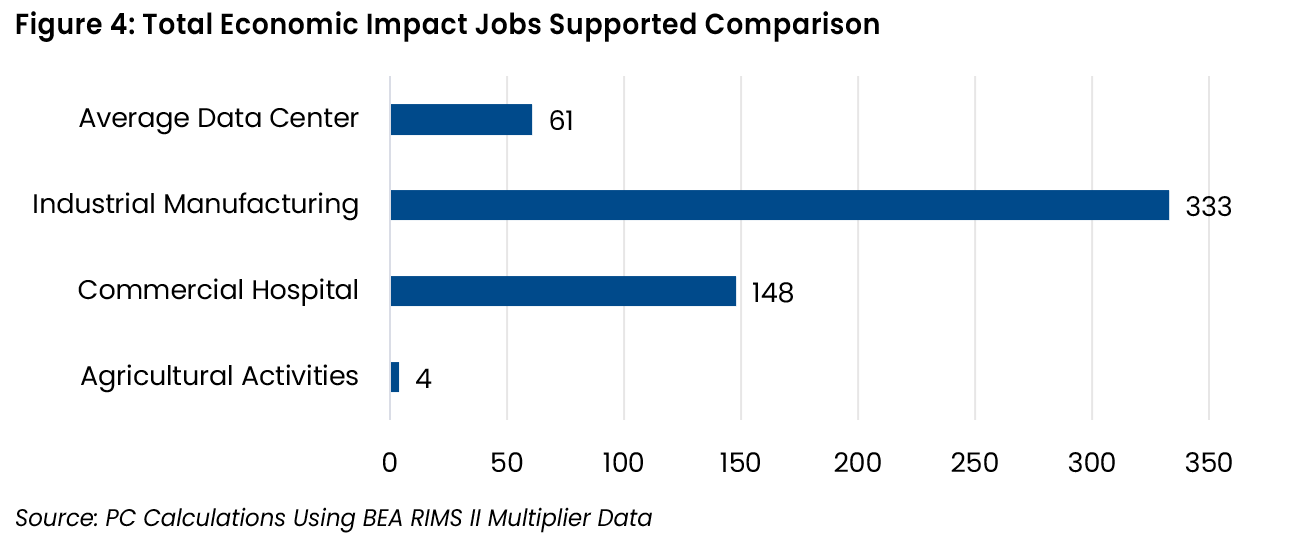

After accounting for multiplier effects, the final results do not change substantially. Manufacturing and health care still produce greater overall economic impacts than an Average Data Center when looking beyond total tax impacts. Using the direct jobs estimates (Figure 2) and the direct effects jobs multipliers (Figure 6), we reached the conclusions presented in Figure 4.

For an Average Data Center, the 35 direct jobs supported result in 61 total jobs supported at the direct and indirect levels (26 additional jobs through indirect effects). In manufacturing, we estimate 333 total jobs to be supported (138 additional jobs through indirect effects). We estimate health care to also support more jobs than an Average Data Center, including indirect effects, at 148 jobs.

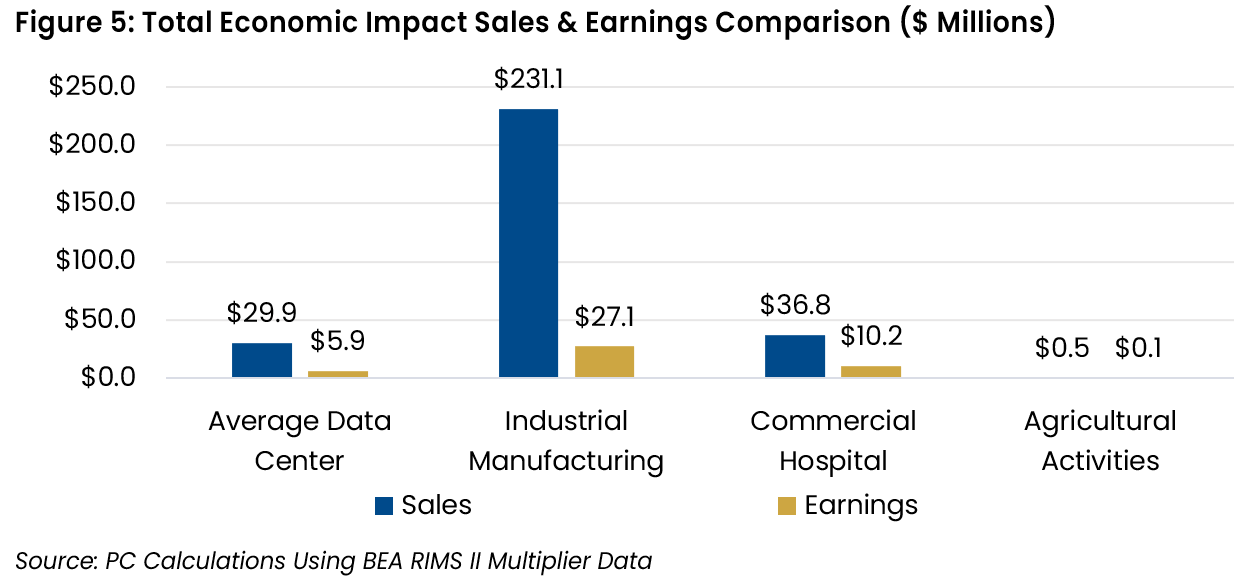

In terms of sales, we expect manufacturing and hospitals to outproduce Average Data Centers, as shown in Figure 5. In total, we estimate an Average Data Center to generate $30 million in sales, adding about $5 million to the direct effects, compared to $231 million for a manufacturing facility (including $53 million added to direct effects) and $37 million for a commercial hospital. We also expect the Data Center to generate less earnings than manufacturing or hospitals at this level.

Multiplier Effects

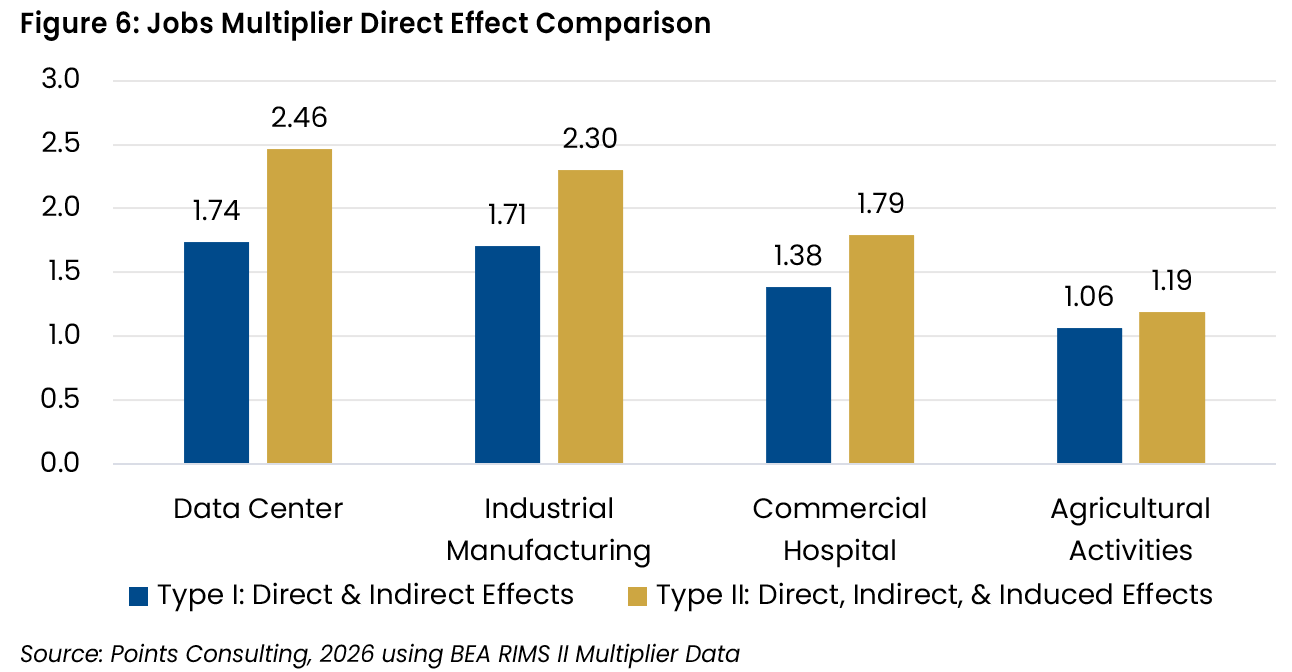

Figure 6 reports the direct effect jobs multipliers for each industry. These multipliers reflect the additional jobs supported across all other industries in the region. Using these multipliers, PC was able to estimate the direct results for output (sales) and earnings. As shown by the multipliers in Figure 6, a Data Center development produces the largest multiplier effects. To be specific, each direct job created by a Data Center supports an additional 1.74 jobs at the Type I level in the local economy (Ellis County in this case), compared to 1.71 for manufacturing, and 1.38 for health care.

Conculsion

In terms of what development to encourage in your community, there is no one size fits all answer. Every new development and industry comes with its own set of pros and cons. In the end, the most important thing is to do your homework to understand what those pros and cons are, because it’s much easier to mitigate the cons if there’s a plan in place from the get-go.